Maritime Chokepoints & the Changing Logic of Conflict in the Gulf

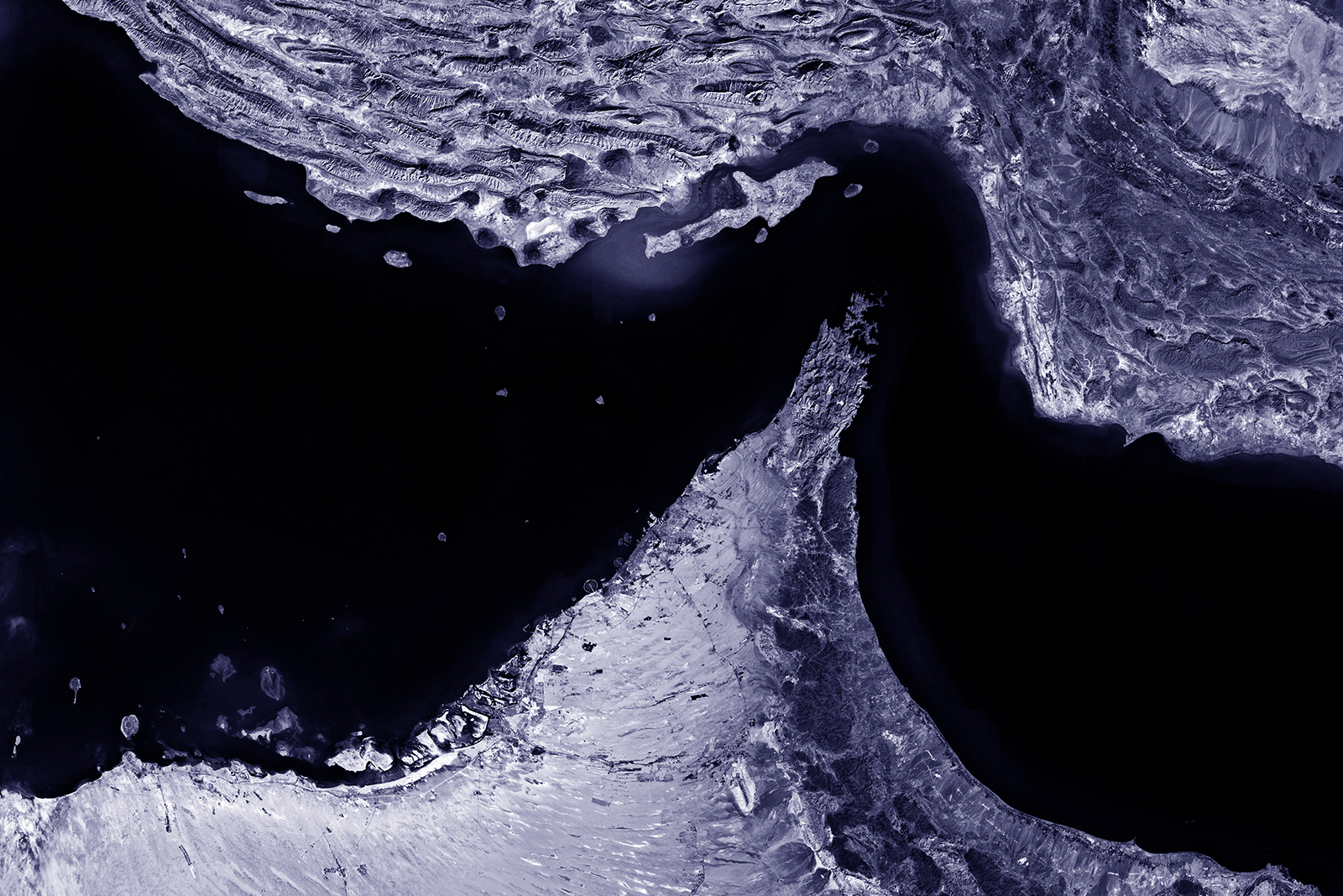

As the war with Iran is entering its third month, the opportunities for a timely and long-lasting resolution of the conflict remain slim. Even though both the United States (US) and Israel have reduced the scope of their armed attacks in Lebanon and Iran, neither side appears willing to commit to a long-term ceasefire. Moreover, the passage through the Strait of Hormuz remains disrupted by both Iran and the US.

What the Strait of Hormuz crisis indicates is that both the US and Iran could achieve their immediate objectives without escalating the conflict militarily. The defining feature of the current crisis is the capacity of the parties to disrupt global economic flows through maritime chokepoints and use this as a source of economic and diplomatic leverage. Even though the Hormuz crisis has severely disrupted maritime traffic and brought sharp increases in oil prices, periodically reaching over 100 dollars per barrel, both sides view the blockade of the Strait as critical for attaining their immediate military and security priorities. Understanding the security and economic ramifications of the US-Iran conflict is paramount to understanding both the behavior of the parties in the conflict and the strategic options for the Gulf Cooperation Council (GCC) states.

THE CHANGING NATURE OF THE CONFLICT

In March 2026, there were credible reports that the US was preparing for a ground invasion of Iran. 2,200 marines from the 31st Maritime Expeditionary Unit were deployed to the Strait of Hormuz together with thousands of soldiers from the US army’s 82nd Airborne Division, which is typically used for rapid seizures in hostile environments. However, mediators from Oman and Pakistan were able to de-escalate the situation, heading off any imminent invasion. Nevertheless, commentators remain skeptical whether the parties really want to de-escalate or are merely making preparatory moves for broader operations.

Those who predict that the conflict in the Middle East will escalate militarily may underestimate the changing nature of contemporary conflict. The disruption of maritime traffic through the Strait of Hormuz is generating pressure far beyond the immediate conflict zone, contributing to higher energy prices, inflationary pressures, and increased volatility across global markets. These economic effects are not confined to regional actors but are increasingly felt by major importing economies and financial markets worldwide. As the economic costs of disruption rise, policymakers face stronger incentives to seek de-escalation and avoid prolonged instability that could deepen recession risks. In this context, the strategic importance of maritime chokepoints lies not only in their military value, but in their ability to shape political decision-making through economic pressure and uncertainty.

THE ECONOMIC IMPLICATIONS OF THE STRAIT OF HORMUZ CRISIS

The real risk for the global economy, while the conflict is ongoing, is the potential for long-term disruptions of oil and gas production and the maritime shipping routes. While the Iraq-Türkiye Crude Oil Pipeline, Saudi Arabia’s East-West Pipeline and the Abu Dhabi Crude Oil Pipeline could serve as alternative routes, they do not have the capacity to fully make up for the disruption of the traffic through the Strait of Hormuz. Land pipelines are also an easy target for hostile drone attacks, as happened with the Saudi East-West Pipeline that was hit by a drone strike on 8 April. In the absence of viable shipping alternatives, any enduring disruption of maritime trade will have long-lasting economic implications.

The Executive Director of the International Energy Agency, Fatih Birol, called the war in Iran “the largest energy security threat in history,” noting that more than 80 energy facilities have been damaged in the course of the war and that restoring their productive capacities is likely to take around two years. Crude oil production has also rapidly declined in the GCC, with Kuwaiti oil output plunging 53% compared to the pre-war level, and the UAE’s by 44% over the course of one month. A rapid increase in the oil and gas prices, combined with the limited capacities of the OPEC countries to rapidly expand supply – especially if traffic through the Strait of Hormuz is disrupted in the long run – increases the risk of an oil shock and stagflation similar to the one in the 1970s.

Economic stagflation is not the only risk; the disruption of the Strait of Hormuz traffic is negatively impacting food security. The GCC states are major producers of nitrogen fertilizers, including urea and ammonia, with Saudi Arabia, Qatar, Oman, and Iran being responsible for around 30% of global fertilizer production. Unlike oil, the fertilizer sector does not have internationally coordinated strategic reserves, and as a result, the prices of granular urea in the Middle East increased by 20% between February and March 2026. Higher fertilizer prices and low supply are likely to lead to a reduction in crop yields for the 2026–2027 seasons in regions like Southeast Asia and the Sahel, where farmers can no longer afford necessary inputs. Lower agricultural yield, combined with higher prices and limited government ability to cushion the inflationary pressures, could create political instability for the Middle East and beyond.

HORMUZ AS LEVERAGE

Prolonged disruption to maritime trade is politically and economically costly. The Strait of Hormuz crisis is a test for the resilience and stability of the international political economy. However, both the US and Iran are seeking to use the disruption of maritime trade through the Strait of Hormuz as a source of leverage.

For Iran, the crisis may present an opportunity to reshape aspects of international petroleum trade, while also creating broader incentives for regional and global actors to reconsider existing energy, trade, and financial arrangements. Iran is seeking to establish a yuan-based toll for oil shipments through the Strait of Hormuz, which challenges the status of the US dollar as the primary currency on the global energy

market. This is putting pressure on the GCC states to divest from US treasuries and assets, increasing the economic costs for both the US and the GCC.

Beyond a theater for economic leverage, the disruption of Hormuz traffic could further drive the escalation of tensions between the parties, but it could also provide incentives for diplomatic engagement. On 17 April, Iran declared the passage through Hormuz open to all maritime vessels; a claim that was later walked back while the US maintained its naval blockade. As Iranian oil output has fallen by 60% between February and March, and with the Iranian currency having already fallen rapidly against the US dollar before the war, the Iranian government is left with little income to fund its war efforts. The US blockade of the Strait thus increases the economic costs for Iran which could bring Tehran to the negotiation table.

Recent developments further illustrate the fragility of the current pause in escalation. In recent days, Kuwaiti authorities reported a drone attack targeting northern border posts originating from Iraqi territory, while Iranian media also reported explosions and aerial interceptions during the ceasefire period. These incidents, despite limited clarity regarding attribution, demonstrate how quickly tensions can re-emerge even amid diplomatic signaling and temporary restraint. The persistence of such events

complicates efforts to sustain confidence in ceasefire arrangements and reinforces uncertainty across regional trade, shipping, and energy markets.

INTERCONNECTED SYSTEM

Global maritime trade is an interconnected system, and the Strait of Hormuz is not the only chokepoint. Seeing Iran’s success in Hormuz, the Houthis in Yemen have also threatened to close Bab al-Mandeb. A simultaneous disruption of trade at both Hormuz and Bab al-Mandeb will cripple trade to both Europe and Asia. Even if Iran and the Houthis do not have the resources to maintain the blockade in the long run, the constant possibility that passage may be restricted, disrupted, or threatened at short notice is enough to deter commercial transit, particularly once insurers are unwilling to underwrite the risk. This alone is sufficient to create pervasive uncertainty in global energy trade, which will lead to shipment delays and require the reorganization of the international trade routes. Higher transport costs are transmitted across supply chains, affecting the costs of both agricultural and manufacturing goods, further adding to the inflationary pressures produced by the high oil prices.

REGIONAL RESPONSES AND IMPLICATIONS

Thus far, the Gulf States’ response to the crisis is a form of strategic restraint. The Gulf States are sending a clear message that they do not support any escalation of the conflict between Iran and the US, be it economic or military. Strategic restraint also positions the GCC states as actors seeking to protect the status quo and resisting the attempts of both Iran and the US to use the disruption of maritime trade as a source of leverage.

For the Gulf States, the Hormuz crisis is not only a threat to their oil and gas revenues. It also provides them with opportunities for building leverage and cementing their centrality in the global trade of goods. Saudi Arabia and Egypt already announced the construction of a new logistical corridor through the Red Sea, which is likely to reduce the dependence of the Gulf States on the trade passing through both Hormuz and Bab al-Mandeb. The route is expected to have a deflationary effect on the Gulf economies by reducing the time and cost of shipping to and from the Gulf. The Gulf states could also invest in expanding the land oil and gas pipelines to China and the rest of Asia. Although such a solution has steep initial investment costs, it could provide opportunities for deepening the trade and commerce between the Gulf states and the Asian industry powerhouses such as China and India. Additionally, the more strategic investments India and China have in the Gulf, the more diplomatic pressure those countries will exercise upon Iran to seek peaceful resolutions to its disputes with the US instead of disrupting maritime trade.

CONCLUSION

The central lesson from the current conflict in the Gulf is that the sources of friction between the parties are not primarily about Iran’s policies in the Middle East. The most consequential feature of the war is no longer the prospect of direct military escalation, but the growing ability of the parties to manipulate maritime chokepoints and thereby disrupt the global economy. Disruption to energy infrastructure and trade routes produces inflationary pressures, supply chain instability, and food insecurity across the globe that can put the world economy into long-term depression similar to the 2008 financial crisis. For the Gulf states, however, the conflict provides opportunities to become more economically resilient as they seek pathways to diversify their energy partners and build new energy ecosystems which are less dependent on maritime trade through either Hormuz or Bab al-Mandeb. What is needed today is economic leadership and strategic restraint that the Gulf states are more than capable of delivering.

The statements made and views expressed are solely the responsibility of the author, and do not represent Fiker Institute.